Strategy's STRC

Michael Saylor's Bitcoin buying machine

TLDR:

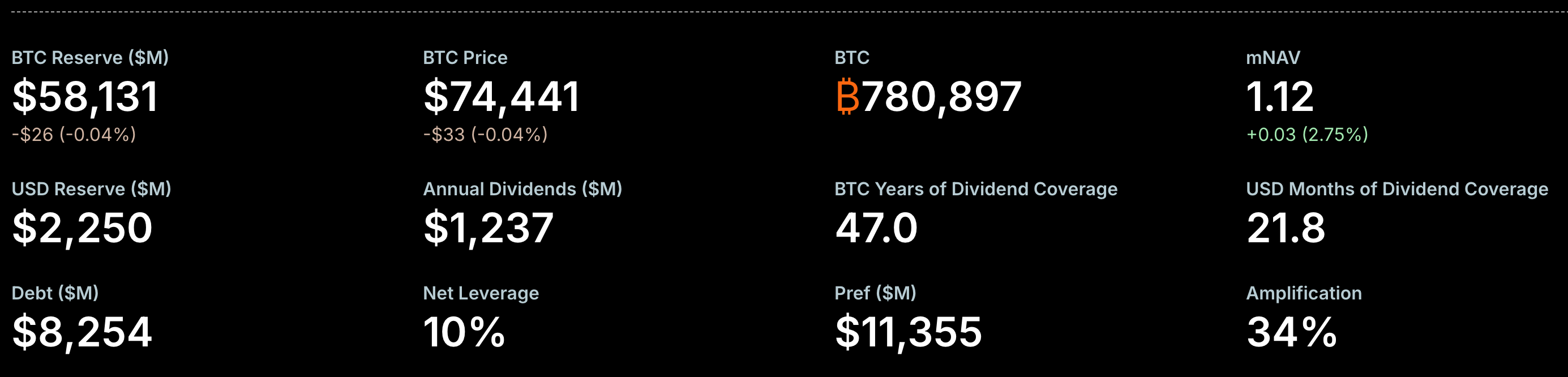

Strategy holds 780,897 BTC and has built four new financial instruments to keep buying more: STRC, STRK, STRF, STRD, a.k.a Stretch, Strike, Strife, and Stride.

STRC is a perpetual preferred stock paying ~11.5% annual yield, designed to trade stably at $100. It’s equity not debt, so Strategy never has to return the principal.

The yield is funded by a $2.25bn USD reserve continuously topped up by new STRC investors, with their huge BTC collateral sitting behind it all.

The risks are real as Strategy carries a $1.24bn/year yield obligation that keeps growing, while buyers can only exit via the secondary market with no guarantees.

STRC and its brothers have introduced novel mechanisms for Strategy to accumulate even more BTC, yet they’ve also brought new risks to the company.

I’ve discussed Michael Saylor and his company Strategy (previously Microstrategy) in a full post back in 2024, and I’ve also mentioned him in many posts since including a post last year where I spoke about Digital Asset Treasury companies, the model created by Saylor.

In recent weeks Strategy have been outpacing all other corporate Bitcoin buyers with a specific financial instrument they created called STRC, which works in a very interesting and different way from their main historic buying strategy, so I decided to discuss STRC today.

If this post resonates with you and you enjoy the content then please share it with a friend and get rewarded for doing so!

This blog goes out weekly to over 20,000 subscribers. Please message me if you’re interested in sponsorships or partnerships.

Strategy

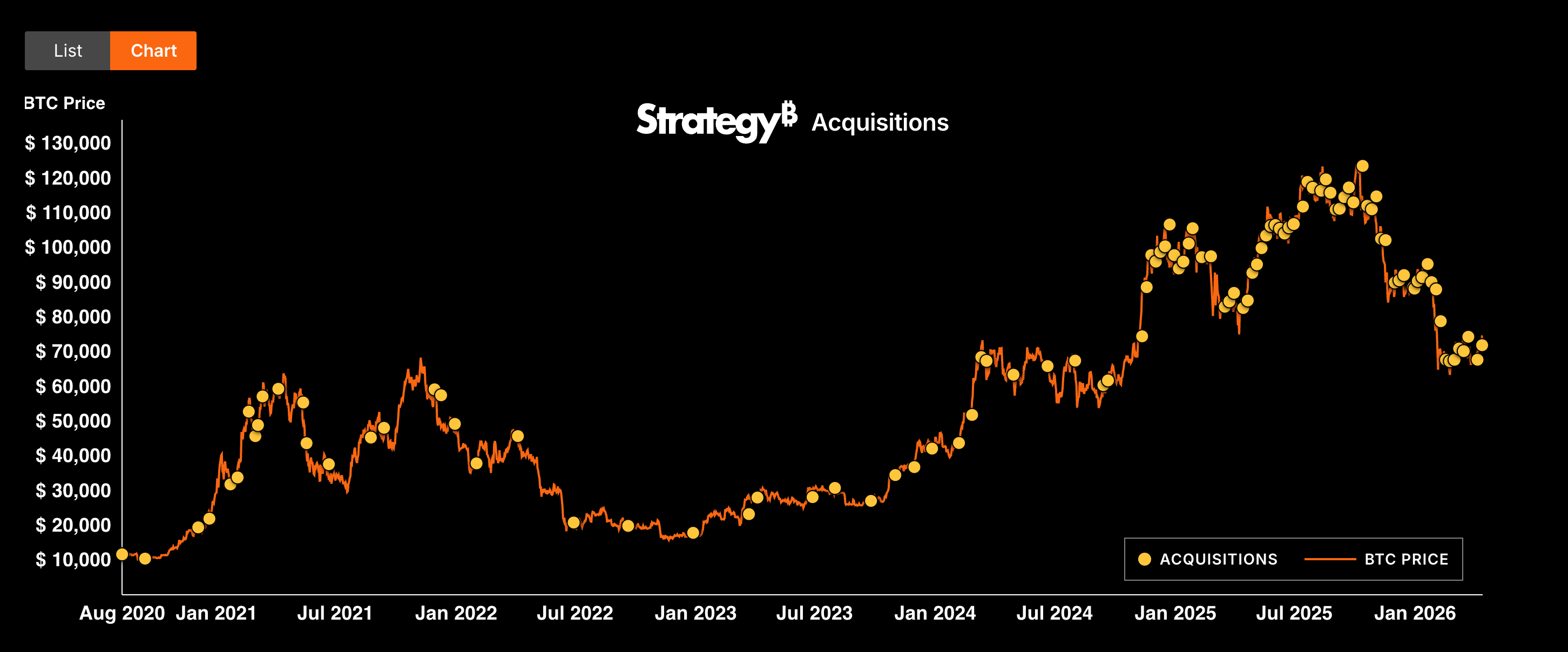

Michael Saylor has one goal: Buy Bitcoin, as much as possible for as long as possible. I’ve covered his company Strategy (previously MicroStrategy) in a post I made a couple of years ago where I explained how he used convertible debt and company equity, through his stock MSTR, to continuously grow Strategy’s BTC holdings.

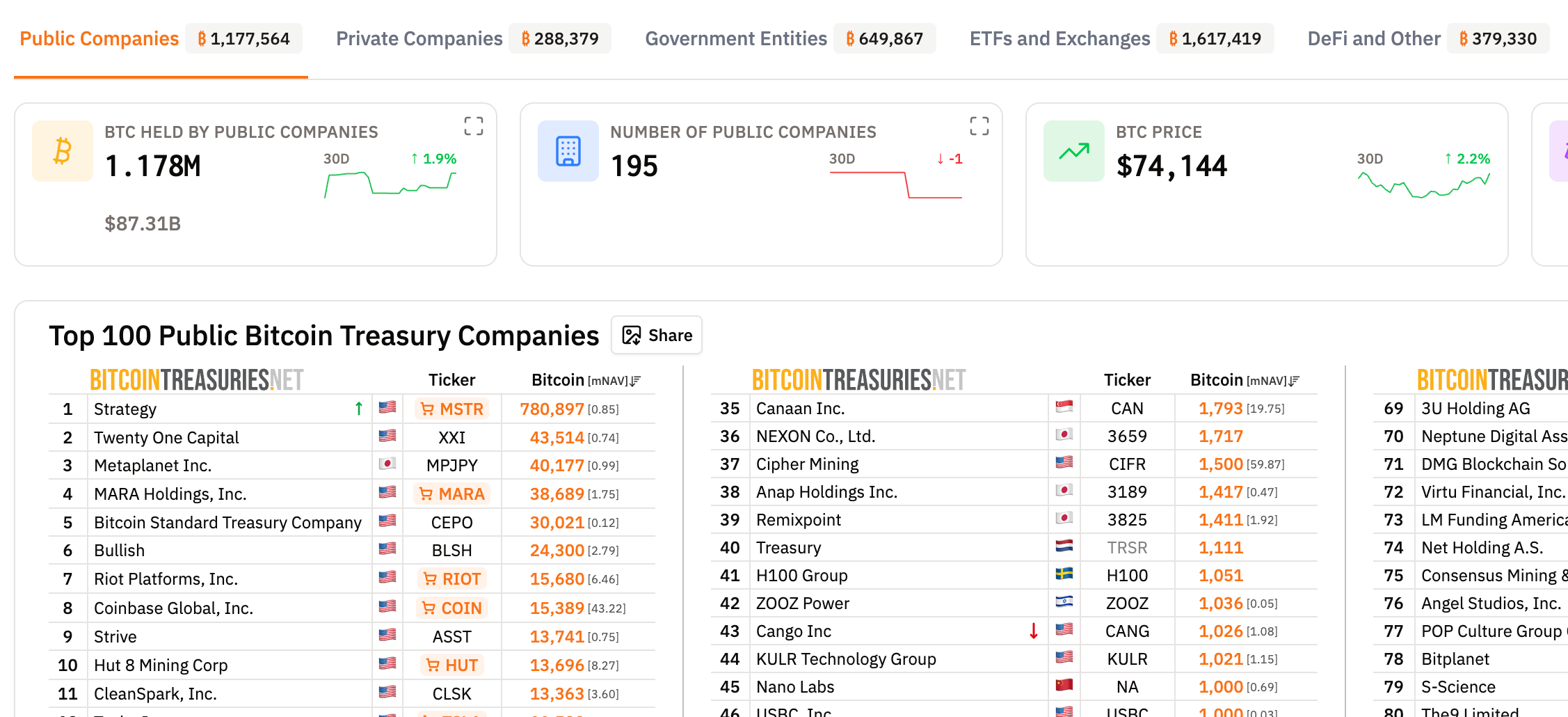

Through this method his company now holds 780,897 BTC, worth around $57bn at current prices and is aggressively moving towards their goal of owning 1M BTC, which would be around 4.7% of all 21M BTC that’ll ever exist.

Strategy created the concept of the Digital Asset Treasury, of which I’ve also written a post before. It’s a formula that’s since been copied by many other companies, and they sit firmly at the top position with this model as you can see on the site bitcointreasuries.net.

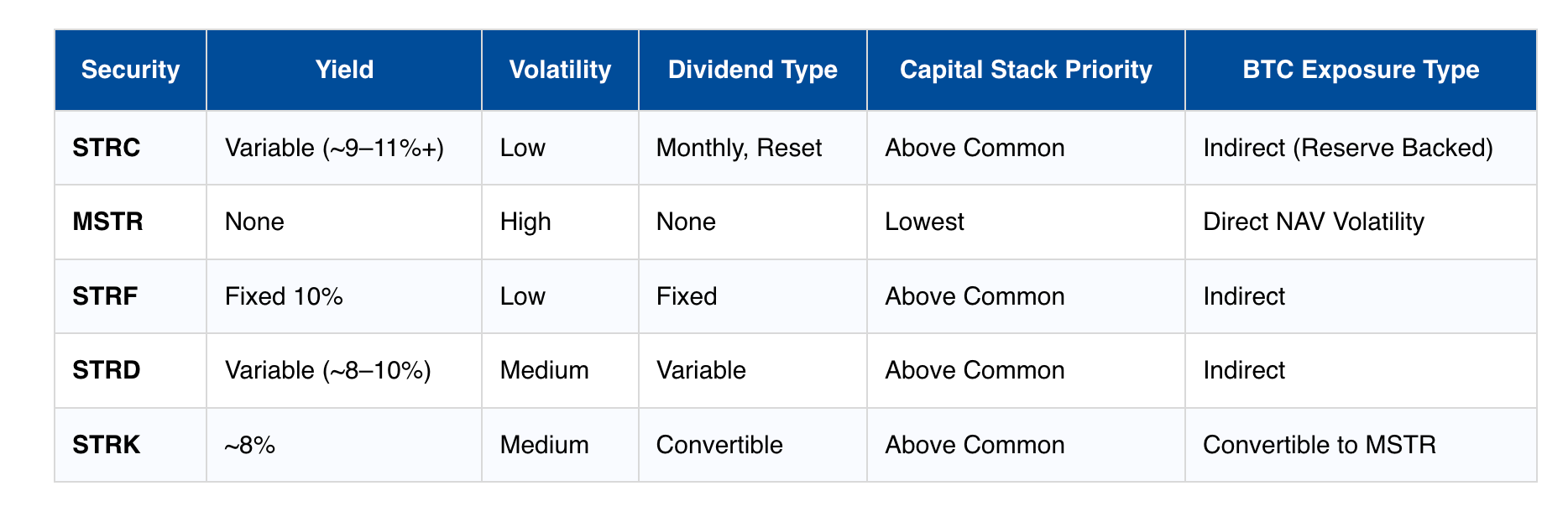

To accelerate their BTC Treasury growth further Strategy has built a suite of 4 additional financial instruments that sit above their common MSTR equity in terms of preference. These are STRC, STRD, STRK, and STRF, pronounced Stretch, Stride, Strike, and Strife.

STRK pays a fixed 8% annual yield and can be converted into MSTR shares, giving holders potential exposure to Bitcoin’s price alongside the yield. STRF pays a fixed 10%, is the most senior instrument in the stack (meaning it has highest preference in a dividend or liquidation scenario), it’s designed for their more conservative investors.

STRD also pays a fixed 10% but sits at the bottom of the preferred stack, making it the highest-risk of the four. And then there’s STRC, which pays a variable rate that’s ~9-11.5% annually, paid out monthly in cash. STRC is the instrument growing the most right now and so it’s the main focus of today’s post.

What is STRC?

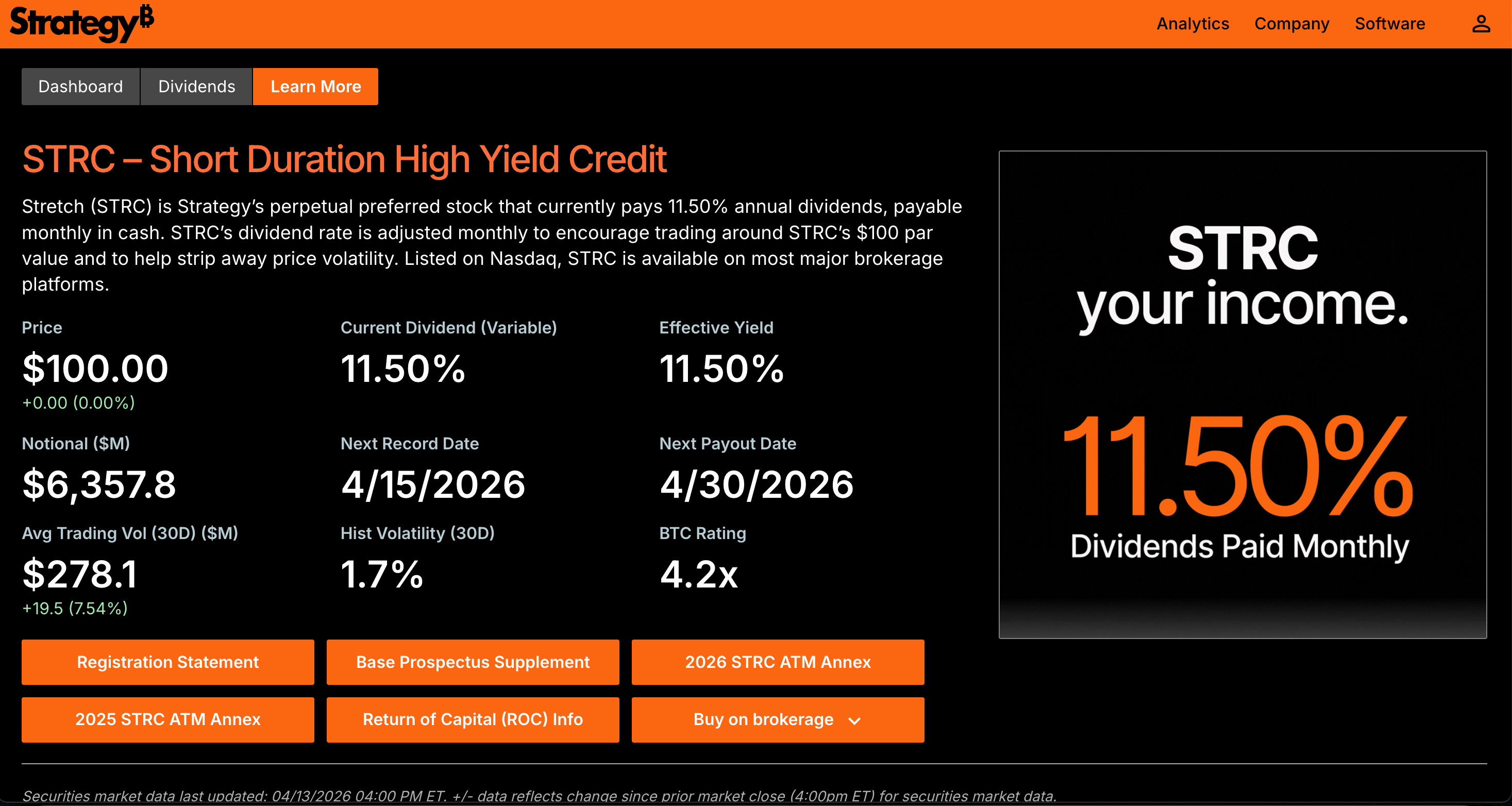

STRC is a perpetual preferred stock listed on Nasdaq. This means it represents equity in Strategy, gets preferred preference on dividends and liquidation, and is perpetual meaning that it never reaches maturity! It’s currently paying 11.5% annual dividend in cash monthly and you can buy it on most major stock exchanges.

The appeal from the outside is simple. It looks and feels like a high-yield savings account. You put in $100, you collect roughly $11.50 a year in monthly payments, and the $100 price tag is controlled so that it doesn’t move. In the last 30 days it’s managed to keep to just 1.7% volatility, while by comparison BTC’s has had around 40%!

Unlike buying MSTR though, you get no exposure to Bitcoin’s price. MSTR might double when Bitcoin runs hard while STRC will just sit stable at $100 sending you a monthly dividend. This is a financial instrument for those that want a more high-risk savings account rather than exposure to Strategy’s BTC treasury.

There is one important thing to remember though here: STRC is equity, not debt. And since it’s “perpetual” it never matures so there’s no end date, hence Strategy has no legal obligation to ever return your $100 principal! The only obligation Strategy has is to pay the dividend, and even that’s actually paid “when and if declared by the board.”

This is a crucial point to understand and we’ll discuss it more further down.

How STRC works

The variable rate mechanism is what makes STRC different from a standard stock.

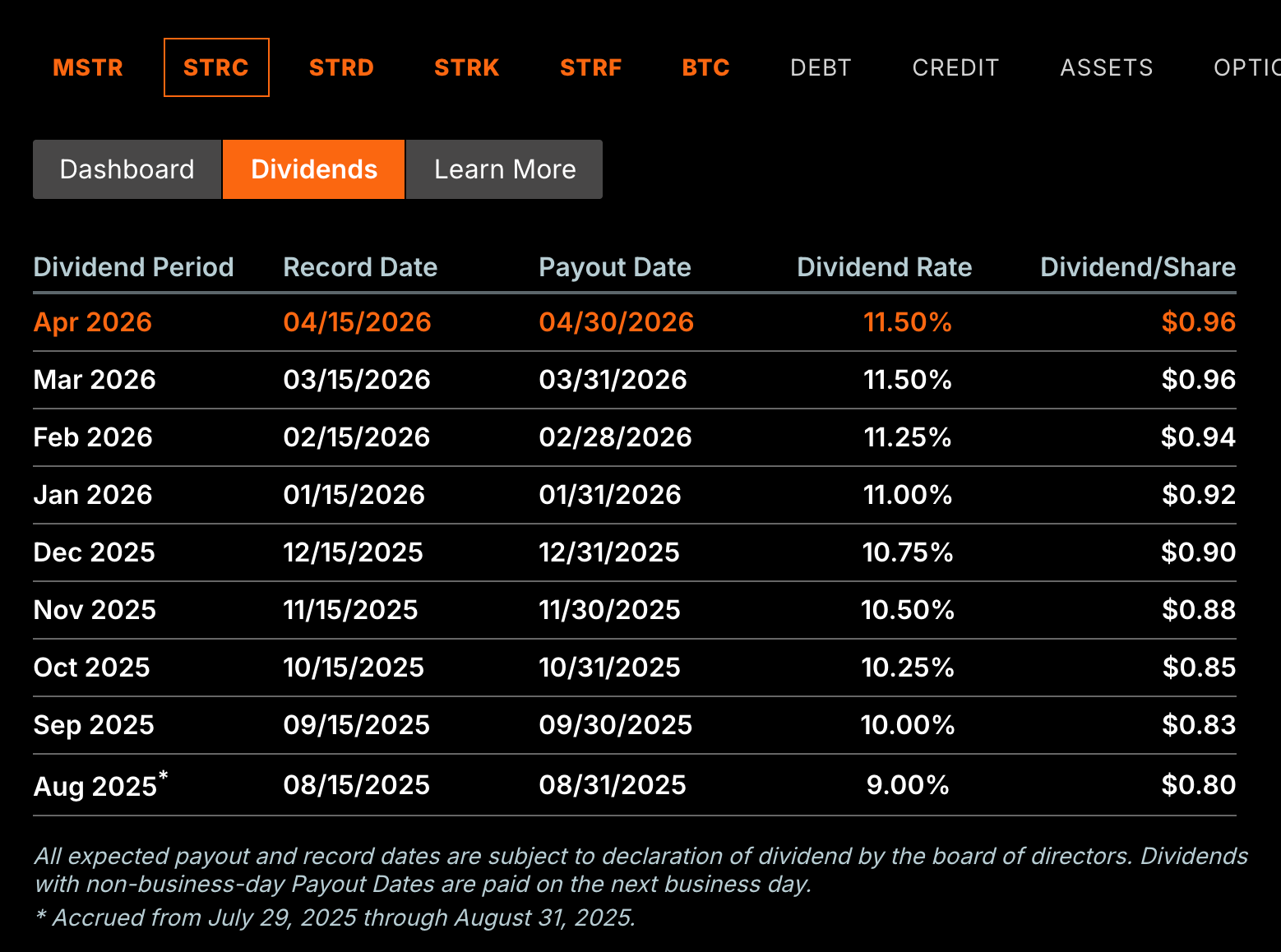

Each month Strategy’s board reviews where STRC is trading relative to its $100 target. If the price has slipped below $100, they nudge the dividend rate up by 0.25% to make it more attractive and create more demand for it. If it has crept above $100, they nudge it down.

Changes are gradual, capped at 0.25% per month, but the goal is always the same: to keep the price anchored as close to $100 as possible, and the mechanism has been working! STRC has held its $100 value remarkably well since launch.

But where does the 11.5% in yield actually come from?

Strategy maintains a dedicated USD cash reserve specifically to cover dividend obligations. That reserve currently sits at $2.25bn, which would cover 21.8 months of dividend payments across all four preferred instruments we mentioned above, as the total annual dividend bill across all 4 is now around $1.24bn per year.

The reserve doesn’t just slowly drain down as dividends go out though, it gets continuously replenished through what is called an “ATM” (at-the-market) offering, where Strategy sells new STRC shares to new investors at $100 each on an ongoing basis.

Some of the USD that Strategy receive when selling STRC gets added to their USD cash reserves, while the rest goes straight into buying more Bitcoin!

The machine tries to sustain itself purely through new investor capital, which honestly feels quite “ponzi-like”, although Strategy has its massive BTC holdings sitting behind everything as the ultimate collateral and so far they’ve never had to sell any BTC to fund dividends.

At current prices, Strategy’s 780,897 BTC represents 46.2 years of dividend coverage at the current payout rate. STRC specifically carries a “4.2x BTC rating”, meaning the Bitcoin backing STRC is worth 4.2 times the $6.36 billion of STRC in circulation.

The Risks

Here is where it gets less comfortable for both sides of the trade.

Unlike the convertible notes that made Strategy famous, which converted into MSTR shares and therefore reduced the company’s debt obligations over time, these preferred instruments have no maturity date. There is no point at which Saylor pays them off or people reduce their debt position voluntarily.

For Strategy, the 11.5% yield is a permanent and growing obligation, that’s already grown to $1.237bn per year across all four instruments and continues to grow. This is an open-ended commitment that expands every time they issue more STRC to fund more BTC purchases.

For the buyer, the risk picture is also quite complicated. You cannot sell your STRC back to Strategy nor will that position ever mature such that they return your money. If you want to exit your position, you need to find another willing buyer on Nasdaq at whatever the market price is.

Under normal conditions with STRC sitting at $100, that’s straightforward. But if confidence in Strategy broke down, probably from a severe BTC price drop, the STRC price could fall and you’d be left holding the bag. Yes you’ll keep getting the dividends but that’s not much comfort if the underlying asset’s price is cratering.

The numbers that ultimately matter most are then Strategy’s debt obligations along with the price of Bitcoin and the quantity of BTC they hold, as these show if they still have enough collateral to cover their debts.

With Strategy’s current debt obligations at ~$8.25bn, and their 780,897 BTC, the BTC price must remain above $10,600, which it is comfortably above at around $65,000-$75,000 in recent weeks.

Meanwhile their preferred stock has a different kind of risk. The $11.355bn across STRC, STRK, STRF and STRD never needs to be repaid, Strategy is not on the hook for that principal. Their real preferred obligation is the $1.237bn per year in dividends, and that keeps growing as long as these instruments exist!

The stress test here is if BTC falls hard enough that new investors stop buying STRC at $100, in which case the ATM machine would slow down and the $2.25bn reserves would deplete over time until they could not repay dividends. There’s no exact BTC floor price for this though it’s more of a general confidence game.

The honest summary then is that STRC and its brothers introduce more risk vectors than Strategy’s earlier convertible debt model.

Strategy now carries a large permanent yield burden with no exit, while buyers carry liquidity risk with no guaranteed floor. The whole construction is a lot more precarious than the clean $100 price and steady 11.5% APY monthly payment make it seem.

Why it matters and what to watch

Whatever your view is on the risk profile, STRC is moving serious amounts of Bitcoin off the market.

It funded 75% of a $1.57 billion Bitcoin purchase in March 2026. On April 13th this week, a $1 billion BTC acquisition was funded entirely through STRC sales. Strategy today holds more Bitcoin than any other entity in the world, and at current rates they could reach 1M BTC before the end of 2026.

The broader point is structural. Saylor has shown that TradFi financial instruments, preferred stock, ATM offerings, yield products available on every major brokerage, can be redirected toward Bitcoin accumulation at a scale that was previously unimaginable.

The mechanism is genuinely novel. A TradFi investor buys STRC on Nasdaq, and their capital flows directly into Bitcoin within days. This connection did not exist before Strategy built it.

The numbers to keep an eye on are whether BTC price ever drops to around $10.6k, at which point their debts would outstrip their collateral, but this was always something to be careful with Strategy. Additionally though you must now look at whether their annual yield repayments ever become larger than their USD reserves.

Neither of these seem likely in the current market, but it’s impossible to predict what’ll happen in the years to come and with these newer financial instruments growing Strategy has certainly created a more risky setup for itself than it had before.

Whenever you’re ready, these are the main ways I can help you:

Want high returns? Earn up to 14% APY with Yieldseeker!

Love Web3 & AI insights? Follow @afoxinweb3 on X!

New to crypto? Join our beginners community to master crypto fast!

Building a Web3 app? Get our expert product development support!