Earning Yield with Lending Protocols

A look at Aave, the top DeFi lending protocol

TLDR:

Lending protocols are one of the most common DeFi protocols. Aave was the first of its kind and is still the largest with over $20bn in total value locked (TVL).

These protocols allow people to anonymously lend/borrow money with each other over the Internet. To protect funds you can only borrow less than you’ve lent.

Whenever you lend the protocol pays you interest fees, and when you borrow it’ll charge you interest. The difference in this interest is how it makes money.

Aave and Kamino both offer great rates on stablecoins. If you’ve got a bunch of cash and want to earn an easy 10%+ then you can supply it to a lending protocol.

BTC surpassed $100k! An incredible moment and mark in crypto history!

We’re in the mania phase of crypto’s cycle with token prices shooting up all over the place. It’s a joyous albeit very distracting time.

We’ve still got a long way to go before this part of the cycle ends. But when it does you’ll want to know where to park your cash to earn some yield. So today I decided to take a look at how to do this with lending protocols.

Read on to learn more, and if you want to continue the conversation then jump in here: beginners.tokenpage.xyz.

Watch the Video version of this Post

Lending Protocols

The crypto space massively evolved when smart contracts were introduced in 2015 with the release of Ethereum. Smart contracts allowed developers to build complex financial applications and gave rise to Decentralised Finance (DeFi).

EthLend was one of the early DeFi projects founded back in 2017 by Stani Kulechov. It was created at a time where people were still getting to grips with what was possible with smart contracts and DeFi on the whole. EthLend’s first version was really awkward to use and looked a bit like this:

However, they continuously upgraded it, and eventually rebranded to Aave, really pioneering the idea of a “lending protocol”. And today they look a lot more modern and hold over $20bn worth of assets:

Aave’s lending protocol has been such a huge success that there have since been hundreds of other lending protocols replicated and recreated for different chains. DeFiLlama has it’s own category for lending protocols and estimates over $52bn of value locked among them all of them across all chains - that’s a lot of money!

A lending protocol is exactly what it says on the tin. It’s a DeFi protocol that allows you to lend, and therefore also borrow, money.

DeFi protocols work in an automated way through smart contracts. So you’re not actively lending to an individual, you’re lending to the protocol itself (ie. the smart contract code), with the protocol setting varying lending and borrowing rates. We’ll take a little look further in the next section.

Since Aave is the largest lending protocol by TVL (total value locked) by a long-shot, we’ll look at it primarily. And since these protocols have expanded to pretty much all smart contract blockchains, we’ll also look at Kamino who are the biggest lending protocol on Solana.

How they work

When you are still new to crypto/web3, lending protocols seem like a really hard idea to grasp. But once you’ve gotten a little more hands on and are used to DeFi, they become one of the simplest DeFi protocols to make sense of.

Picture them a lot like borrowing money from a bank. You can borrow $100,000 to buy a new house but you’ll need to put collateral down (like the house itself) that will be reposessed if you don’t repay that loan. Plus every month you’ll need to pay back some % interest on top of your borrowed amount until you’ve paid it all off.

In Aave you do the same, except you’re not dealing with a bank, you’re borrowing directly from the protocol itself. And the protocol allows you to take out the loan in any of the tokens available for a given “market”, where these tokens have been lent to the protocol by another person who’s also using the protocol.

![Lending protocol framework [11] | Download Scientific Diagram](https://substackcdn.com/image/fetch/$s_!k1jC!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F739d0ce0-0a7c-4de6-afb5-288ea8fc81d6_714x463.png "Lending protocol framework [11] | Download Scientific Diagram")

So for example, you may lend 1 ETH valued at $3,500 and then use that as collateral to take out an over-collateralised amount of $3,000 USDT. With that you USDT you can spend it as you like, but you’ll need to keep paying the interest until you decide to pay that $3000 back, at which point you can once again pull out your ETH collateral.

If the price of 1 ETH goes up to say $5000, you’ve still got your 1 ETH, as well as the interest earned from supplying it to the protocol. And when you’re ready you can pay back the interest charged on your USDT plus pay off the $3000 USDT loan itself.

However, if that ETH goes down in value, then you may fall below a minimum collateral threshold and be liquidated. Meaning Aave will take your ETH collateral from you to make up for the $3000 in USDT that you still hold, so they don’t end up out of pocket.

The main way lending platforms make money is then through the spread (ie. difference) on the returns they give when you lend money vs the interest they receive when you borrow it!

If that still sounds a little confusing then follow along as we look at Aave below.

Lending on Aave

Aave’s already on it’s third version (V3) and they support several Ethereum compatible L2 chains. So the first thing you need to do is select the chain you want to lend on. That’s done simply by selecting the “market” from the drop down:

If we look at Ethereum for now you’ll see that there’s 4 assets you can supply, namely ETH, WETH, DAI, and sDAI. Yet there’s over 30 assets you can borrow in return!

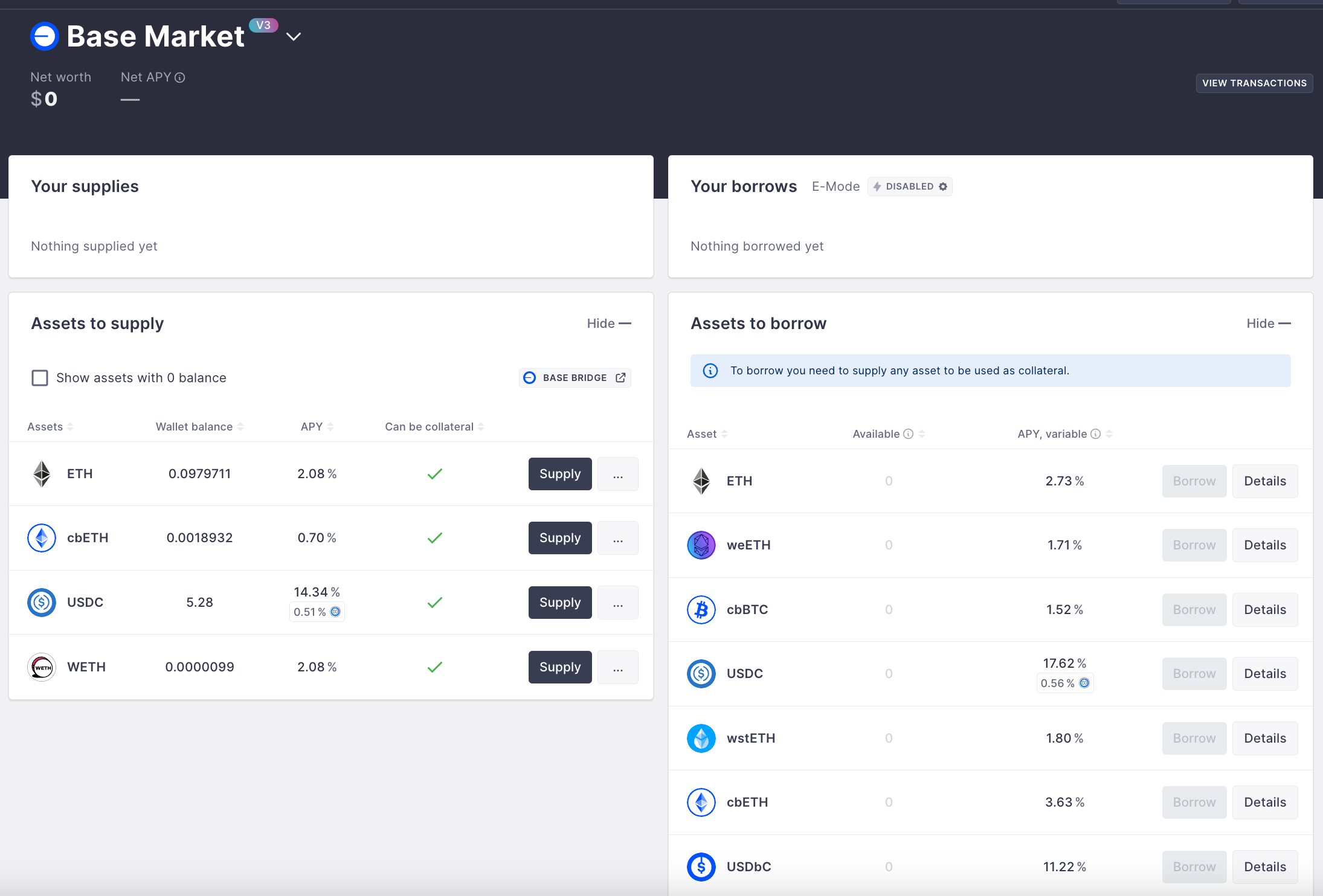

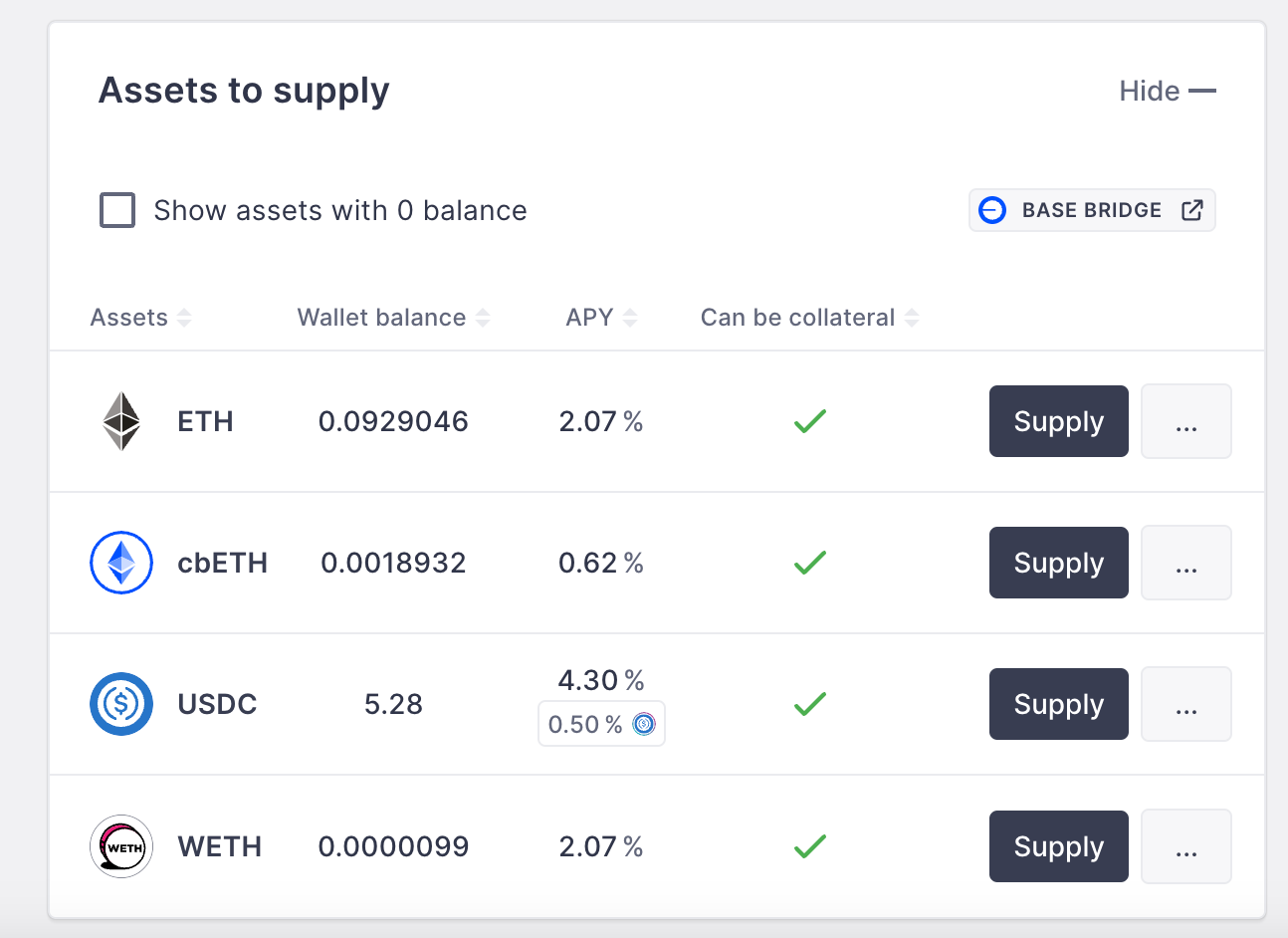

However, for the sake of simplicity let’s go over to Base market, where there are fewer tokens to reason about and the fees are really low.

You can see the Aave interface is super simple. On the left hand side it shows you the different currencies you can supply and on the right-hand side the ones you can borrow. But remember, you can only ever borrow if you’ve already supplied, because the platform needs to over-collateralise what you will borrow.

So let’s run an example, and say I provide ~$20 in ETH on Base. First I select the Base market, then select “supply” for ETH. At today’s prices 0.005 ETH is around $20.

Then I just hit “supply ETH”, sign the transaction, and it’s done! And I’ll start earning 2.06% return for the year ahead on my ETH.

I’m also given an aToken (ie. Aave token), in this case aBasWETH (ie. Aave Base Wrapped ETH) that represents the interest bearing ETH.

Borrowing on Aave

Now that I’ve supplied ETH as collateral, I can use that $20 in ETH that I have on Aave to borrow another coin.

So say I want to borrow some USDC (Circle’s USD stablecoin), then I can just select Borrow, and Aave shows’s a limit of around $15 so that I’m over-collateralised with a good margin of $5.

Borrowing close to the limit increases your chance of being liquidated if the price of ETH has a sharp fall, and they even put a warning to let you know.

Now that I’ve borrowed USDC, you can now see both how much I’m supplying and how much I’m borrowing at the top of the screen.

As you can see above I still have $19.34 worth of ETH on Aave, but I’m losing -10.19% in interest at the moment, and I have a dangerously low “health factor” since I’m very close to the limit of being liquidated as I’ve already used up 96.96% of my borrowing power!

When that number hits 100% then I’ll get liquidated and Aave will take all my ETH collateral away from me.

In particular you can see this even clearer by clicking on “Risk details”. If ETH drops only a tiny bit more then I’ll hit the 83% liquidation threshold - ie. I’ll be liquidated when the $15 I’ve borrowed is worth more than 83% of the ETH I’ve supplied.

It’s best to never let your “health factor” get so low, so when you see these sorts of numbers above you should realistically either supply more money or repay what you’ve borrowed to avoid being liquidated.

Earning Yield on Aave

Now you’ve seen how to lend and borrow on Aave, so it’s clear that when you borrow you need to pay off the interest, however when you lend you are actively earning interest (ie. yield) on the money you’re supplying!

Therefore earning yield through a lending protocol is as simple as supplying it money.

However, different markets and different coins will give you different APYs (Annual Percentage Yield). And these APYs are constantly changing based on the lending protocol’s specific algorithm, which is not necessarily easy to interpret. So the APY you are earning today may be different by tomorrow.

So for example, if we take a quick look in Aave, at today’s rates the Base market will give a 4.3% return on USDC. This is similar to what US treasury bonds are currently offering.

However, if I go into Aave’s Polygon market, I can see they are offering 15.05% on USDT and 15.87% on DAI. These are pretty hefty returns for USD and I’m not aware of any US banks offering this sort of return!

So if I supply $10,000 in USDT and the APY remains at this level of 15.05%. Then I’ll earn $1,500 over the next 12 months!

This in particular becomes very interesting when people have very large sums of money. Because for example with $1m you can be earning $150,000 annually, or around $400 per day, for just lending your money to the platform!

That’s pretty good by most standards, although admittedly Aave’s algorithm will likely rebalance that APY down over time. As an exemple a couple of days ago we had a bizarre spike where Aave was giving over 38% on USDC, but that didn’t last long.

As a side note, the return for supplying Base ETH today is around 2.07% APY, while borrowing it is costing around 2.73% APY. This difference between borrowing and lending is the spread that Aave earns as a profit.

Earning Yield on Kamino

Every lending protocol works roughly the same, they’ve all copied Aave’s core formula, but it’s still worth taking a quick look at Kamino which is the largest lending protocol on Solana.

Currently they are giving around 14.23% on USDC, 20.18% on PYUSD (Pay Pal’s USD stablecoin) and 25.24% on USDT.

This is even more generous than Aave’s markets and with the same numbers as above if I supply $10,000 in USDT and the APY remains at 25.24%, then I’ll earn $2,500 in the next 12 months. Meanwhile if for example I supply $1m in USDT, I could be making $250,000 annually, or around $680 per day!

So as you can see, supplying money to a lending protocol can be an incredibly lucrative endeavour.

Risks

Now nothing in life is without it’s risks, no lending protocol is giving out money without getting something in return.

The first thing to take into consideration is that, as we said before, the APYs are variable so you may be getting a great return today and then find a few weeks or days down the line that it drops massively and ultimately it was a bit of a pointless exercise.

The bigger risk though comes when you consider the old saying “not your keys, not your coins”.

Any money you leave on a lending protocol you can be easily pull out. However, ultimately it’s not in your custody any more, the money is now in the protocol’s custody.

Protocols are pieces of automated code that obey rules. But these rules can be subverted by either a malicious hacker or even a malicious developer who wrote the code in the first place! So any money you have on a lending protocol is subject to the risk of being hacked and therefore entirely stolen.

However, in the cases of both Aave and Kamino they have time on their side. The longer a protocol has survived without being hacked or being an outright scam, the less likely of either happening.

So at least with Aave and Kamino you can assume you’re relatively safe.

To conclude, now you know how to earn yield by supplying money to a lending protocol. It’s simple as it is effective, especially with stablecoin markets.

Nonetheless, it’s not for everyone. It really depends on your goals and the sorts of risks you’re willing to take. But it’s a good thing to know about and understand, as the more you know about the space the more informed decisions you can make with your own money.

Whenever you’re ready, these are the main ways I can help you:

FREE access beginners.tokenpage.xyz - Get a free video guide on how to set up your first wallet and buy your first crypto. Plus a 1-on-1 call with me for free, and $1,990+ of bonus course material.

VIP access beginners-vip.tokenpage.xyz - Get VIP access with me as I show you how to navigate crypto’s. Includes weekly Q&A calls where you can ask me anything, and our proprietary DeFi portfolio software.

Web3 software development at tokenpage.xyz - Get your Web3 products and ideas built out by us, we’ve built for the likes of Zeneca, Seedphrase, Creepz and more.